Top 10 Forex News and Analysis – Mar 01, 2023 Mar 01, 2023 Mar 01, 2023 Mar 01, 2023

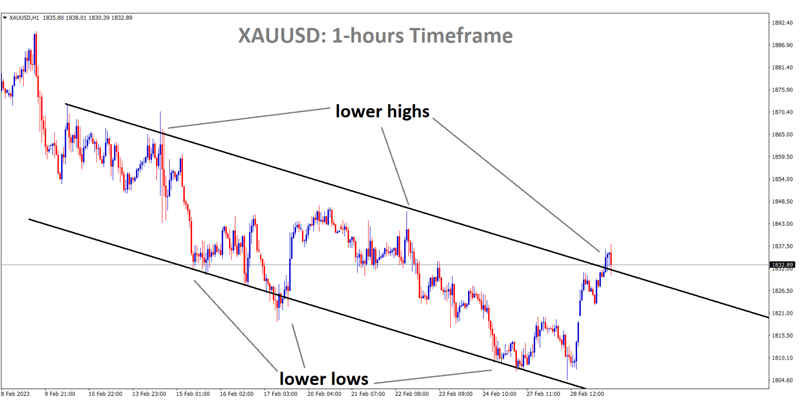

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel.

The positive readings of China’s Caixin and NBS Manufacturing PMIs for the month of February keep the Chinese economy’s development shining despite the lockdown periods.

This bodes well for gold prices because China is the world’s largest consumer of the precious metal. Chinese Minister Liu recently stated that his country was prepared to revive its economy through fiscal expenditure.

The Federal Open Market Committee (FOMC) will take its cues for March from domestic statistics from the United States.

With a three-day winning run beginning early Wednesday in Europe, the gold price is off to a strong start in March, with a recent intraday high near $1,835. As XAU/USD continues its upward trend above $1,823 and is joined by news related to China, the recent rally appears logical from both fundamental and technical viewpoints.

The world’s largest industrial player and one of the main Gold consumers has seen an economic rebound in recent months, as evidenced by the positive prints of China’s Caixin and NBS Manufacturing PMIs for February and the Non-Manufacturing PMI for the same month. The data prompted China’s finance minister, Liu He, to signal his country’s willingness to increase government expenditure while also noting the unsteadiness of the groundwork for China’s economic recovery. Meanwhile, Gold buyers have been able to maintain control of the market thanks to mild losses in the US Dollar Index (DXY) following the largest monthly advances since September 2022.

However, the XAU/USD exchange rate appears to be under surveillance due to hawkish worries regarding the US Federal Reserve (Fed) and fears of a further inflation crunch in the future. After initially mirroring Wall Street’s light losses, S&P 500 Futures turn positive, reflecting the prevailing sentiment, while US Treasury bond yields stay higher as of late. Moving forward, next week’s key US jobs report will be preceded by the February S&P Global and ISM PMI details, both of which will be essential for immediate directions. Gold investors must pay close attentionto the Federal Reserve meeting in March and Chairman Jerome Powell’s remarks.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

The US Consumer Confidence report came in at 102.9, which is lower than the 108.5 that was predicted. With inflation at record highs and interest rates on the rise, the economic outlook for the United States looks bleak.

As disappointing data was released, the US dollar gauge fell against its major trading partners.

In February, a popular measure of U.S. consumer attitudes deteriorated substantially for the second consecutive month, indicating that Americans are becoming more pessimistic about the economic outlook in the face of persistently high inflation and rapidly rising interest rates.

According to the Conference Board, consumer confidence fell to 102.90 in February from a downwardly revised 106.00 in January, missing consensus estimates for a modest rebound to 108.5 and reaching its lowest level since November 2022.

The present situation index, which is based on the assessment of business and employment market conditions, increased to 152.8 from 151.1, but the expectations indicator, which measures short-term prospects for income, the business environment, and employment opportunities, plummeted to 69.7 from 76.00 previously.

USDCHF Analysis

USDCHF is moving in an ascending channel and the market has fallen from the higher high area of the channel.

The GDP in Switzerland came in at 0.0% in the first quarter, down from 0.30 percent in the fourth quarter and 0.2 percent in the third. Due to higher inflation and rate hikes, Swiss retail sales on the board and the Swiss Franc failed to satisfy the market. Before the release of the US Domestic data collection, USDCHF is continuing to consolidate.

As bulls take a breather early on Wednesday after February’s strong performance, the USD/CHF retests its intraday bottom at around 0.9410. As a result, the market’s mellow pessimism about the Swiss currency combination due to worries about rising interest rates and inflation is not justified. Data from the world’s biggest industrial player, China, showed impressive performance in February, so the country may be to blame.

However, official activity data as reported by NBS’s Manufacturing and Non-Manufacturing PMIs indicate that China’s economy experienced a significant uptick in February, as measured by the Caixin Manufacturing PMI. However, after the release of the data, China’s finance minister Liu He said that the economic recovery in China is not yet based on a solid basis.

It’s worth noting that the USD/CHF bears appear to be favoured by the month-start consolidation and the lately softer US data. Consumer confidence in the United States fell for the second straight month in January, falling to 102.9 from 106.0 (revised) and the US Housing Price Index falling 0.1% in December from -0.6% market forecasts and -0.1% in November. In a similar vein, annual growth in the S&P/Case-Shiller House Price Indices was 4.6% in the month in question, below the 6.1% predicted by the market and the 6.8% seen in the month prior. In addition, the Richmond Fed Factory Index dropped below 11.0 in February from -5.0 expectations and 11.0 in January, and the Chicago Purchasing Managers’ Index fell to 43.6 from 44.3.

However, market concerns about inflation and rising interest rates have kept USD/CHF purchasers optimistic. The S&P 500 Futures mirror the sentiment of the market by following its slight losses on Wall Street, which are currently hovering around 3,960. The yield on the 10-year US Treasury bond increased by two basis points (bps) to 3.93% as of press time, while the yield on the 2-year US Treasury bond increased by four bps to 4.84%. As a result, both of the most important bond coupons are heading in the direction of the three-month peak set in February, which was the result of the largest monthly gain since September 2022.

In addition to the risk-averse sentiment, disappointing domestic statistics may give USD/CHF buyers reason to remain optimistic. In comparison to the previous two quarters’ increase of 0.3% and 0.2%, Switzerland’s GDP in Q4 of 2022 came in at 0%.Ahead of the United States’ January economic statistics, USD/CHF movements may be influenced by Switzerland’s Real Retail Sales for the month. Federal Reserve (Fed) Chairman Jerome Powell’s testimony and the Federal Open Market Committee (FOMC) monetary policy meeting next week will, however, be watched closely for clear guidance.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Spanish and French inflation readings were greater than anticipated, which helped the EURUSD in th markets.

Keeping the Euro against counter pairs in a strong positive frame of mind are the Chinese Caixin and NBS manufacturing statistics.

The most anticipated event in the market is the ECB’s Next Move rate rise at the following meeting; this domestic data will prompt a 50bps increase in the market rate in the coming weeks.

Prior to Wednesday’s European session, EUR/USD resumes bids to retest an intraday peak close to 1.0595. However, prior to the recent corrective bounce, the major currency pair experienced its worst monthly loss since last September.

The Euro pair does this while experiencing a month-start sluggish session and pre-data anxiety, taking cues from the wide US Dollar pullback. It’s important to note that the positive inflation reports from Spain and France support the EUR/USD recovery along with China-inspired favour. That said, the early readings of Spanish and French Consumer Price Index (CPI) details for February marked upbeat outcomes and bolstered the hawkish worries surrounding the European Central Bank’s (ECB) next move on Tuesday.

Contrarily, the US Housing Price Index declines 0.1% in December versus -0.6% market forecasts and -0.1% prior, while the US Conference Board’s (CB) Consumer Confidence drops for the second straight month to 102.9 from 106.0 prior (revised). Additionally, the February reading of the Chicago Purchasing Managers’ Index eased to 43.6 from 44.3 previous readings and 45.0 market expectation, while the February reading of the Richmond Fed Manufacturing Index eased below 11.0 from 11.0 prior and -5.0 expected to -16.

It should be noted that robust readings for February from China’s Caixin and NBS Manufacturing PMIs join the corresponding month’s Non-Manufacturing PMI to signal an optimistic economic recovery in the world’s largest industrial actor and favour the risk profile. The basis of China’s economic recovery is still unstable, however, according to Liu He, the finance minister of China, who spoke after the data was released.

In light of this, S&P 500 Futures start out following Wall Street’s slight losses before turning positive. The US Dollar remains on the bull’s radar, though, due to the firmer US Treasury bond yields, the Fed’s hawkish wagers, as well as the problems with global inflation. Despite this, the US Dollar Index (DXY) is still slightly down near 104.85 despite February’s strong north-run. In the near future, the Harmonized Index of Consumer Prices (HICP), Germany’s primary inflation measure, could present a challenge to the pair’s upward momentum if it fails to meet the optimistic 0.7% MoM forecasts, compared to 0.5% previously. The February S&P Global and ISM PMI data are also crucial to pay attention to.

EURCAD Analysis

EURCAD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Goldman Sachs predicted the ECB would raise interest rates to 50 basis points and 3.75% in June, which was 25 basis points higher than the prior estimate of 3.5% in June. The ECB has already stated a 50bps rate increase in March, consecutive rate hikes of jumbo numbers continue until 2024, and the ECB maintains 3.85% predictions from money markets. According to recent comments from ECB chief Philip Lane, the ECB will not stop its rate hikes by the end of 2023.

Goldman Sachs increased its estimate for the European Central Bank’s peak interest rate hike for the second time in two weeks, saying it now expects rates to rise by 50 basis points (bps) at the ECB’s May meeting. According to the firm, this would raise the central bank’s terminal rate to 3.75% by June.

The bank previously predicted that the ECB would raise rates by 25 basis points in May, reaching a high rate of 3.5% by June. Money markets anticipate the ECB rate to peak at around 3.85% in December this year. The ECB has increased interest rates by three percentage points since July and has promised another half-point increase in March, hoping that more expensive financing will reduce price growth from levels still above 8%.

Recent data, including an upward surprise in Spanish and French inflation figures, as well as recent commentary from ECB chief Philip Lane, who stated that the central bank will not end rate hikes any sooner, spurred the brokerage’s more hawkish expectation. While a step-down to 25 basis points is still conceivable in May, we no longer see it as the baseline… and continue to believe that the Governing Council will keep the peak rate in place until the fourth quarter of 2024, Goldman Sachs analysts wrote in a February 28 note.

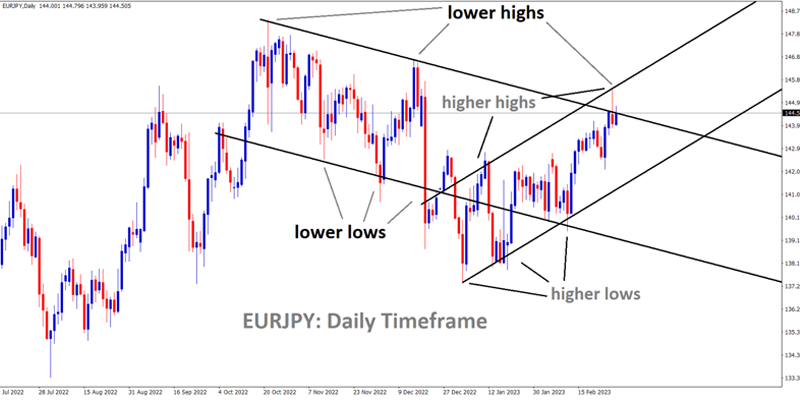

EURJPY Analysis

EURJPY is moving in the Descending channel and the market has reached the lower high area of the channel and the market has reached the higher high area of the minor ascending channel.

Junko Nakagawa, a member of the Bank of Japan Board of Governors, has stated that the country is working towards a more prosperous economic cycle through increased salaries for the general populace. In retrospect, we can see how counterproductive it was to take an ultra-loose monetary policy position in order to boost the economy. At this month’s meeting in March, we focus on analysing the corporate bond market and discussing additional measures to improve market functions.

This time it’s Reuters with some remarks from BoJ board member Junko Nakagawa on inflation and the economy’s future. To correctly assess the current market trend, multiple pieces of information must be considered. We want to see an upswing in the economy that leads to salary increases. When asked whether the Bank of Japan should take additional measures to improve market functions as soon as its March meeting, the BoJ stated that it wanted to spend more time examining the corporate bond market. Though I review the economy at each policy meeting, there may be calls within BoJ to perform a comprehensive assessment of the policy framework.

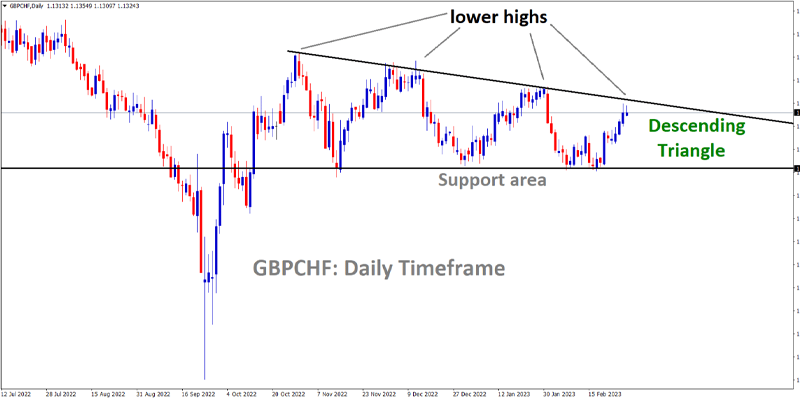

GBPCHF Analysis

GBPCHF is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern.

Even though he has to appease both Conservative Brexiteers and DUP members, UK Prime Minister Rishi sunk remains upbeat about the Northern Ireland Protocol. Goods can travel over Northern Ireland with a green signal from the Windsor framework, but must wait for a red signal to cross over the European Union (EU) portion of Ireland and the rest of the EU.

Tory Brexiteers and DUP members on UK PM Rishi sunak’s side will agree to this stipulation. For the Northern Ireland Protocol deal, this is the tough vote.

Rishi Sunak expressed optimism regarding the specifics of the most recent version of the Northern Ireland Protocol, which regulates the flow of goods from England to Northern Ireland despite the fact that both countries are still part of the United Kingdom.

The new “Windsor Framework” proposed a green lane for products remaining in Northern Ireland and a red lane for goods destined for EU member Ireland and the rest of the EU, which will be subject to more stringent inspections. In order for the negotiated agreement to be accepted, it must appease Tory Brexiteers and the DUP.

The pound has risen against a number of G7 currencies in response to the news of the deal’s advancement, a statement that has not been made frequently in recent times. According to the most recent findings of the Gfk consumer report, the UK’s economic pessimism appears to be diminishing as citizens anticipate an improvement in their personal financial situation over the next few months.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The RBNZ has a sound strategy for raising rates when market inflation figures rise.

According to ANZ Bank analysts, “the move was fairly specific to the Kiwi; unlike on many other occasions, it wasn’t a USD move.” The Kiwi has performed better on crosses, particularly against the AUD, as shown below. Although there was no apparent catalyst, the analysts continued, “as each day goes by, the weight of the data seems to increase in favour of the Reserve Bank of New Zealand needing to do more. The labour market doesn’t appear to be slowing down. It’s also on everyone’s mind, and that suggests volatility, the three-way tussle we mentioned yesterday (between those citing rebuild activity, those worried about the disruption to exports and effect on Crown finances, and those anticipating a USD rebound).

The US rate futures, which have priced in a peak fed funds rate of 5.4% hitting in September, back the bid for the US dollar even though recent important releases have featured some cooler data. Rate reductions this year have almost been put into the market. As a result, the US Dollar indicator, DXY, which compares the greenback to a basket of major currencies, increased by 0.18% in late morning Wall Street trade and was on track to post a gain of over 2.5% in February, the first monthly gain since September.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Canadian GDP figures came in at 0.1% as opposed to the 1.5% forecast and 2.3% in prior months, which was lower than anticipated.

This is a warning indication for the market’s CAD pair prices. The governor of the Bank of Canada stated that tightening monetary policy is sufficient to drive current inflation higher; however, this period’s weak GDP necessitates that the BoC raise rate hikes the following time to maintain lower market inflation.

The Loonie asset’s upward trajectory has slightly slowed down, but the upside bias is still present. The Canadian currency is anticipated to regain its previous week’s peak around 1.3665 as the US dollar continues to strengthen due to growing concerns about the Federal Reserve’s potential for further policy tightening (Fed).

The United States recession has entered the picture amid hawkish Fed wagers, which has led to further losses for the S&P500 futures during the Asian session. Although there are barriers around 104.70 on the US Dollar Index (DXY), the risk aversion motif is still strong. The yields on US government bonds have risen further as a result of investors anticipating a massive rate increase from the Fed in light of February’s economic indicators, which point to an increase in inflationary pressures. At the time of writing, the 10-year US Treasury rates were scaling to 3.94%.

As a result of disappointing Gross Domestic Product (GDP) (Q4) data, the Canadian Dollar is currently confronting enormous offers. The annualised GDP stayed unchanged lower than the 1.5% consensus estimate and the 2.3% reported earlier. While the monthly GDP (Dec) declined by 0.1% versus an expectation of no change. Although flat GDP figures are not necessarily favorable for Canada’s economic outlook, they are advantageous for the Bank of Canada, which is working to reduce persistent inflation. In light of the fact that the present monetary policy is restrained enough to temporarily reduce inflationary pressures, it is important to note that BoC Governor Tiff Macklem has already halted the policy tightening spell after raising rates to 4.5 percent. In the oil market, prices have steadily risen following positive Caixin Manufacturing PMI statistics from China. The economic statistics came in at 51.6, surpassing both the consensus prediction of 50.2 and the previous release of 49.2. It should be noted that Canada is the top oil exporter to the US, and rising oil costs will support the Canadian Dollar.

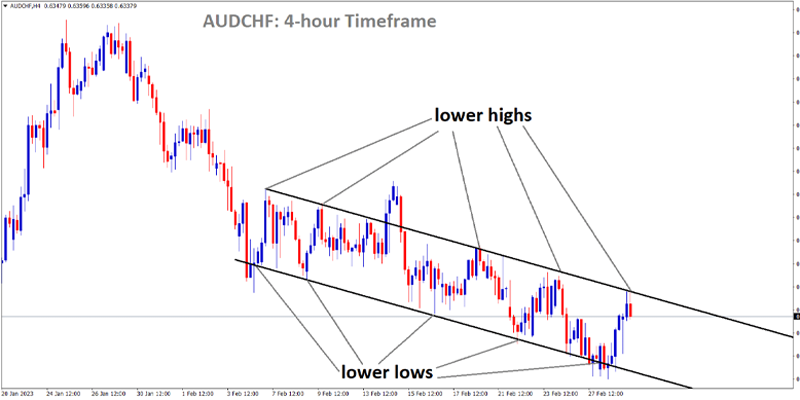

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

GDP for the fourth quarter of the Australian Dollar (AUD) came in lower than anticipated, at 0.50% versus 0.80% forecast. The RBA’s monetary policy interest rate is scheduled to be increased next week; if the increase is 25 basis points, then rates will increase to 3.6%; this will be the eleventh increase since last May. The Australian trade surplus amounted to AUD 14,1 billion, compared to the estimated AUD 5,5 billion. Yesterday’s retail sales data were 1.9% higher than anticipated at 1.5%. Analysts anticipate that all of these scenarios will result in a rate hike at the next RBA meeting, if at all possible.

After the fourth quarter’s GDP came in at 0.5% instead of the 0.8% expected and against the prior 0.7% that was revised up from 0.6%, the Australian dollar fell below 67 cents. Afterwards in the day, the currency rebounded on the back of encouraging statistics from China. As expected, more optimistic adjustments to earlier quarters show that annual GDP to December 31 was 2.7%. It was 5.9% in the previous round.

The GDP numbers released today come in advance of a monetary policy conference next Tuesday by the Reserve Bank of Australia. It is expected that they will raise their cash rate goal by 25 basis points (bp), bringing it to 3.60 percent. That would be the eleventh price increase since the programme began in May of last year. The most recent reading of 7.8% year over year is significantly higher than the RBA’s goal band of 2-3%. The retail sales and current account figures from yesterday serve as the foundation for today’s statistics.

For the final three months of 2018, Australia recorded a current account balance of AUD 14.1 billion, which was significantly higher than the AUD 5.5 billion that had been predicted and the AUD 0.8 billion that had been previously reported. January’s 1.9% increase in month-over-month retail sales beat both the 1.5% forecast and the -4.0% previous. The economic fundamentals are sending mixed signals, but with inflation running rampant, the RBA may have little option but to tighten further in the near future. There’s a lot of fog around the future image, and it’s not clear what to expect. Some lagging signs may signal impending difficulties. The decline in home prices has persisted, and surveys of company sentiment are showing a downward trend.