AUD Markets Await RBA Interest Rate Decision Amid Rising Inflation Amid Rising Inflation Amid Rising Inflation Amid Rising Inflation

EURAUD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

On Tuesday, the Reserve Bank of Australia (RBA) is expected to raise interest rates for the tenth consecutive meeting, despite the fact that economic growth is expected to decelerate and inflation is expected to remain elevated. Policymakers face the difficult task of crafting an appropriate message in light of these projections.

The consensus among economists is that the Reserve Bank of Australia will raise its cash rate by a quarter of a percentage point, bringing it to 3.6%, a level that has not been seen since May of 2012. With weaker-than-expected economic indicators through February, all eyes will be on Governor Philip Lowe to see if he sticks to his advice that there will be further rate rises in the future.

Australia’s Housing Market

A significant decline in the value of the property market in Australia might have severe repercussions for consumers’ spending habits as well as the vulnerability of the nation to enter a recession. Because of this, monetary policy and increases in interest rates are subject to intense scrutiny in the context of the real estate market.

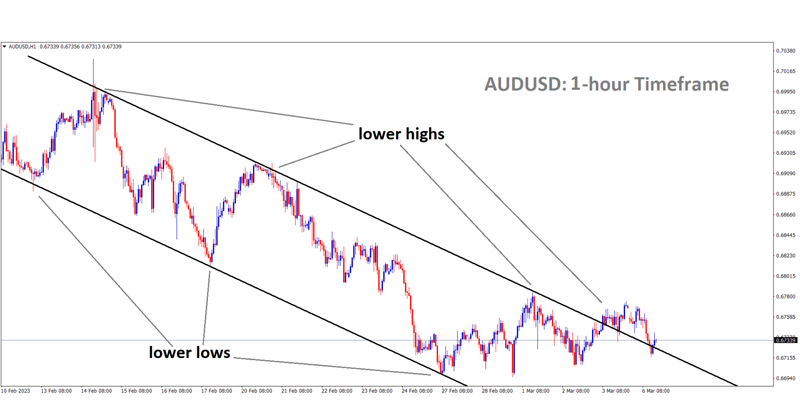

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

When interest rates are higher, mortgage repayments are also higher; this, in turn, might make it more difficult to get financing and diminish the demand for purchasing real estate. Mortgages that cost more money to get might encourage property investors to unload their holdings, which adds to the existing supply of homes and drives down prices. Those who entered the property market when prices were high will now have to pay a higher price for an asset that is worth less than it did when they bought it. This is because interest rates are increasing.

When this is combined with other factors, such as stagnating wages or rising unemployment rates, it can cause people to fail on their debts, which forces them to sell their belongings and further dilutes demand. The combination of increased demand for real estate and a limited supply can push up home prices significantly, but this trend can only be sustained to a certain extent. The property market may decline just as dramatically when potential purchasers are no longer willing or able to pay the increased prices.

Wage Growth Controversy

One of the most significant choices that the present board has made in recent times was the announcement of a rate rise of 0.25 percentage points in May 2022. This will bring the cash rate from an all-time low of 0.1 percent to a rate of 0.35 percent. Since 2010, this was the first time the Federal Reserve had increased interest rates. The fact that there was evidence of considerable upward pressure on wage rise was a significant component of the reason for it.

GBPAUD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The evidence was deceptive, as shown by nearly a year’s worth of official data, which is now available. There was not a significant uptick in the rate of wage growth. Although there have been localized areas of faster wage rise in certain sectors, such as the hotel and food services industries, it is abundantly evident that a significant portion of the bank’s rationale was flawed. It in no way negates the fact that the bank should have increased interest rates. If anything, the desire for robust wage growth may have prevented the board from taking a more dramatic measure to combat inflation earlier.

As we fast forward to September of the following year, we find that the annual growth rate of salaries has increased to 2.2 percent, but the quarterly growth rate is still just 0.6 percent. Inflation is being driven not by wages but by profits, which is bringing the RBA closer to a halt on interest rates.

AUDCAD is moving in an Ascending triangle pattern and the market has rebounded from the higher low area of the pattern.

According to the findings of recent research conducted by the Australian Institute, an increase in the amount of profit earned by corporations in Australia is responsible for more than two-thirds of the nation’s inflation problem. The annual rise in salaries had only increased to 2.3% by the end of 2021, with a meagre gain of 0.7% in the quarter that ended in December.

Australia Export Revenue

As Beijing blocked access to Australian barley, coal, wine, and other exports in 2020, Australia’s trade diversification away from China takes up speed. China is Australia’s largest trading partner. Growth in trade with regional partners that are perceived to be more strategically aligned with Australia is another piece of data that may be taken as further proof of the need for diversification.

It is believed that free trade agreements (FTAs), such as the Australia-India Economic Cooperation and Trade Agreement, and “friend-shoring” programs, such as the Inflation Reduction Act enacted by the Biden administration, would help to solidify the move in the coming years. The latter provision enables businesses located in the United States to qualify for a tax credit if they obtain a certain percentage of the essential minerals used in battery production from inside the country or from a nation with which the United States already has an FTA.

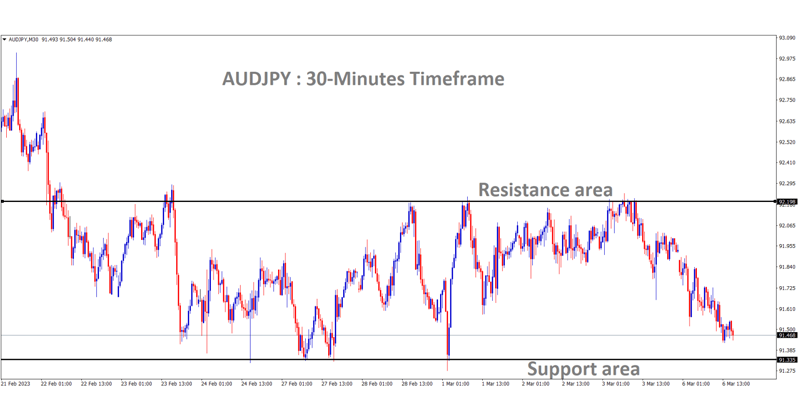

AUDJPY is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

Yet, such stories are unable to account for recent shifts in the proportion of trade shares. The fluctuations in the global price of iron ore can be used to explain the changes in China’s proportion of total trade. Iron ore has continuously contributed more than sixty percent of the value of total commodities exported by Australia to China. Iron ore prices witnessed an exceptional increase over the entirety of the year 2020 and the first half of 2021. According to the data about trade, this resulted in a twelve percentage point increase in China’s share of total commerce. Even though Beijing was obstructing a variety of Australian exports, China’s share of global commerce increased by 6 percentage points despite this fact.

Nevertheless, a downward trend in the price of iron ore began in July of 2021. By the end of the year 2022, China’s trade share had reached the level that was predicted to be achieved if the price of iron ore had stayed at the same level as it was in January 2020. If Beijing were to withdraw the policies that were causing disruption, it is possible that global markets would steer Australian goods back to China. The resumption of coal commerce between Australia and China in January 2023 appears to have signaled the start of this process, which looks to have already begun. The other conclusion is that the geopolitical risk from exposure to the Chinese market has turned out to be very low. Because of this, the commercial case for many companies to invest in diversification is considerably less than is typically indicated.